23 Better Money Habits You Need to Start Doing in 2022: One step at a time and adopting better money habits can help you take control of your finances to start building a brighter future for yourself.

It’s possible that terrible money habits are to blame if you have trouble saving for the future or feel like you’re living paycheck to paycheck. Mint Financial Coaches have shared their best money-saving tips for the new year, and we’ve compiled their advice into a list of 23 new money-saving habits to try in 2022. Save more money and stick to your budget!

What Are Better Money Habits?

In order to reach your financial objectives and improve your relationship with money, you need to adopt healthier money habits. Good money habits can make your life easier, reduce your anxiety about money, and help you save for the future.

Making healthier money habits begins with eliminating your bad money habits and replacing them with good money habits, such as only purchasing when you have a genuine need to do so.

According to Experts, here are 23 ways to improve your money management.

Follow the advice of our Mint Financial Coaches if you’re not sure how to get started creating healthier money habits in your everyday life. You’ll be astonished to learn that you may save more than $900 a year by making your own coffee instead of going to the coffee shop.

Make an effort to improve your credit rating

When you have a strong credit score, you show that you are responsible with your money and are more likely to qualify for lower interest rates on loans. Increasing your credit score will cut your credit card and financing charges’ interest rates and improve your insurance rates.

Even if you don’t have a credit card, you can still utilise it wisely. You can improve your credit score and get incentives by making on-time, complete payments on all of your bills and by charging fixed expenses to your credit card.

2. Decrease Debt on Credit Cards

CPA/PFS, CFP coach Joe Dike says that having a solid money habit can help you pay off debt or even generate an income. As you work to improve your credit score, you’ll save money on interest rates by paying off your credit card debt.

Using a credit card for most transactions can quickly spiral out of control, especially when interest and financing costs are factored in.

Student Loan Repayment Priority

Repaying your students’ loans early in the new year can be a fantastic way to create better money habits and save money in the long run, especially if you have a student loan.

Not being ashamed of taking out school loans is perfectly acceptable. One of Jared Smout, CPA’s biggest financial errors was taking out more school loans than he required. A young family need easy justifications, he explained, “but we could have made more sacrifices instead of carrying an extra financial load.”

Keep an eye on your finances.

The difference between what you own and what you owe is your net worth. This information can assist you in keeping track of your progress as well as your expenditures, as well as teaching you new money management skills. This is an excellent money habit to establish if your goal is to become more financially wise. Keeping track of your liabilities and making sure they don’t outweigh your assets is a great way to get started.

By reducing liabilities or raising the value of assets, good money habits tend to have a favourable impact on net worth.” CPA/PFS Joe Dike CFP, Mint Financial Advisor

To save money, review and reduce your regular expenses.

The end of the month is a scary time for many of us because we’re afraid to see how much money we’ve spent. However, making it a routine to go over your expenses might help you save money by reducing wasteful spending.

Om Mandhana, CFP, a Mint financial coach, shared some ideas on how to save money on everyday expenses:

When you’re at a coffee shop, you can save money by ordering a cup of black coffee instead of a cup of flavoured coffee. Make your own coffee and cut down on the number of times you go out for a cup of joe.

Downsize your data package or switch to a virtual network operator (MVNO).

Running, walking, and hiking — or even cartwheeling — are all free physical training activities you can do at home instead of shelling out money for gym subscriptions and personal trainers. Plan to spend no more than 2% of your annual salary on a gym membership if you still feel the urge to go.

Eating at home and making healthier choices when it comes to food can save you money in the long run. Think about making a big batch of meals in advance and bringing it with you for the week.

Set Up a Savings Account

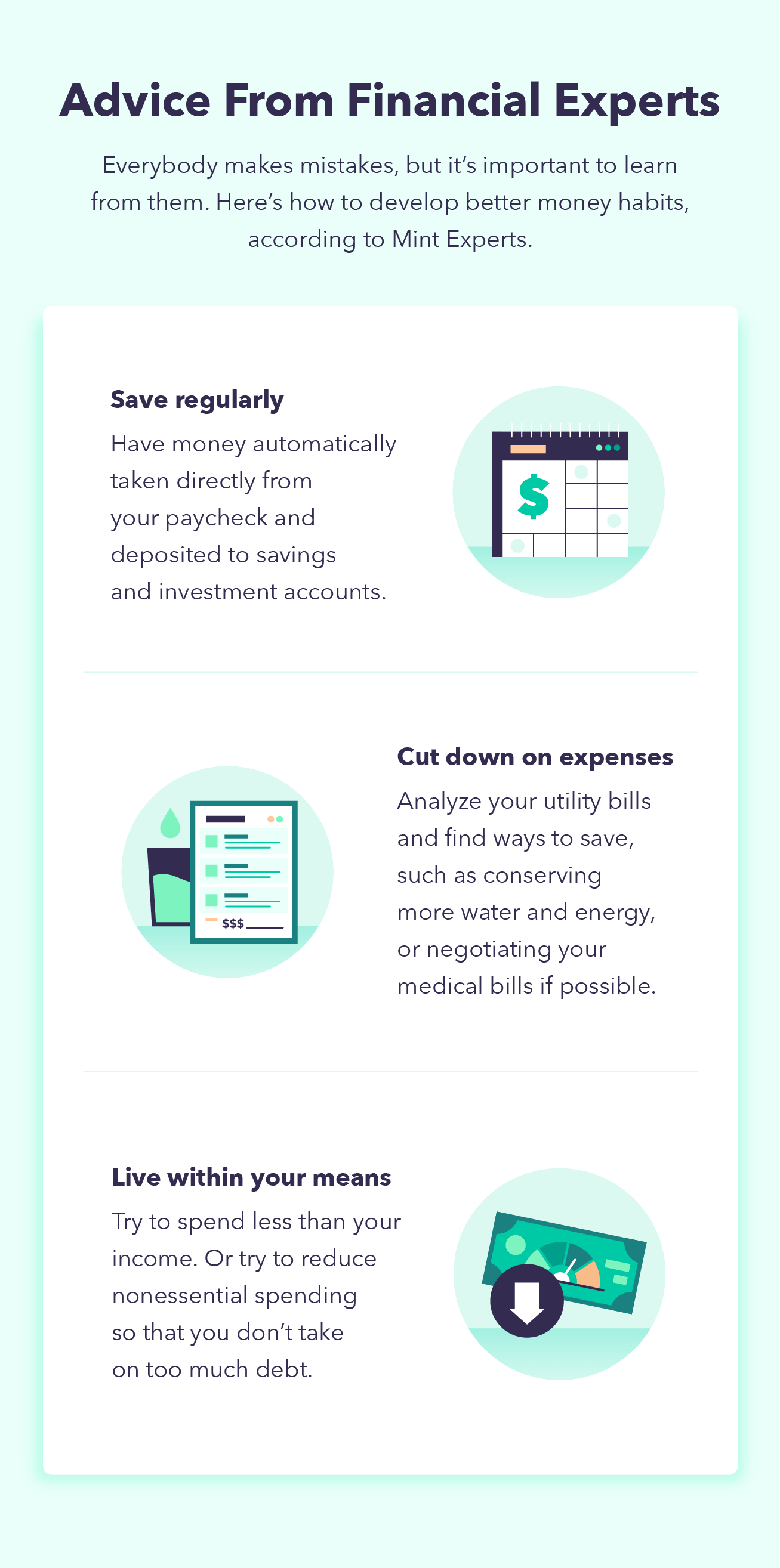

Anthony Castella, CPA, a Mint Financial Coach, emphasises the significance of saving frequently if you want to create better money habits. He stresses the importance of saving a portion of each paycheck for the future. Castella suggests automating the process of saving and investing money by having it deducted from your paycheck on a regular basis.

Dike suggests systematic savings if you currently have a savings strategy in place but wish to improve the amount of money that you save. For this, he sets savings objectives and deadlines, then figures out how much money he needs to save each week or month to meet those goals and automates the process.

Make Time for Your Financial Situation

Good money habits can be achieved if you set aside time each week to focus on your finances. Set aside one day a week to review your finances and identify areas for improvement.

Ralph Schule, CPA, a Mint Financial Coach, has a bottom-up approach to time management when it comes to his finances. Using this method, you keep track of how much money you have leftover each week after paying bills and saving, and you only ever spend what’s leftover, barring emergencies.

Buy Only What You Actually Use

Instead of impulsively buying stuff you don’t need, make it a point to think twice before you buy anything. It’s not really a good deal to buy something if you do not need it, says Karen Layfield, CPA, a financial coach at Mint.com. However, conduct your homework and ask yourself whether or not you really need or want the item before making a purchase.

Even if you don’t need to buy anything, it’s a good idea to hunt for used goods. Make sure to keep in mind that you don’t have to buy the most up-to-date gadgets or clothing, and there are many secondhand options that are just as good for the planet as they are for your wallet.

What I’ve learned about spending money is “Use it up.’” Make sure you’ve given it everything you’ve got. Is there a way to get around this? — CPA Jared Smout, Mint’s Personal Finance Expert

Decide on Your Post-Career Goals

It is never too early to begin planning for the future. Use the 401(k) plan offered by your employer if you can, especially if they match it. As you begin to plan for the future and build better money habits, any bit of assistance is helpful. A portion of your salary will be earmarked for this retirement account, which you can use in the future.

Learn from Your Mistakes in Money Management

It’s inevitable that you’ll make blunders while working to improve your financial habits. You must, however, learn from your mistakes if you hope to improve your relationship with money in the future. Some of our own financial coaches here at Mint have made mistakes in the past and have shared their lessons with us.

Mandhana, for example, learned his lesson the hard way when he lost $5,000 trading currencies on leverage. Now, he’s a buy-and-hold investor, and it’s been working out nicely for him.

Improve Your Financial Literacy

Dike’s money habit of never ceasing to study is an excellent one. In order to become more financially knowledgeable, it is important that you learn about money. Learn how the Mint Financial Coaches stay on top of the latest developments in the financial world and apply what you’ve learned to your own life.

Fidelity Investments’ webpage

Having a subscription to Kiplinger’s Personal Finance Magazine

I’ve been listening to the Faith Driven Investor podcast.

Kitces.com and getAbstract.com subscriptions

YouTube is a great place to find Ray Dalio’s videos.

You can be healthy and affluent if you put your knowledge to good use rather than just accumulating it. CPA/PFS Joe Dike CFP, Mint Financial Advisor

Begin preparing a spending plan.

Making a budget is essential if you want to improve your financial habits. In order to avoid a negative money habit, such as going over your budget, it is vital to set limits, such as a spending limit for groceries, and to keep track of your expenses.

Getting started managing your money may be done in a variety of ways, from using an app to participating in money-saving challenges. The most important thing is to stay dedicated and pick a method that works best for your lifestyle.

Make Use of Discounts and Coupons

Mandhana recommends using discount coupons when making a purchase. Another smart money habit to get into is doing your homework and selecting something that matches your budget. You may save money on groceries by just purchasing foods that are in season and on sale, advises Mandhana. Products can be stored and preserved during the off-season if you have time and room.”

“Select things only when they’re in season and on sale. Store and preserve food throughout the off-season if you have the resources. In the words of Mint Financial Coach’s CFP, Om Mandhana:

Reduce Your Monthly Housing Costs

You may also improve your financial habits by practising them in the comfort of your own home. To save money on utility costs, look for ways to conserve water and electricity or to bargain medical bills. Make a habit of making a shopping list, planning your meals in advance to prevent food waste, and doing price comparisons before you buy anything. Find free activities for the family and reduce subscription services you rarely use if you feel you’re spending too much on entertainment.

How Much Should I Spend on Food?

Avoiding Emotional Spending is a good rule of thumb.

It’s easy to satisfy short-term cravings with unhealthy money habits, adds Dike. Avoid going out when you’re upset or depressed, delete shopping apps, and leave your credit card at home to limit your emotional spending. A few days of contemplation and budgeting will help you decide whether or not to buy something.

Spending without consideration to necessity or emergency is a bad money habit driven by immediate satisfaction. CPA and Mint Financial Coach Ralph Schule

You need someone to keep you on track.

Seek out someone who can hold you accountable if you’re having trouble staying motivated to achieve your goals. Anyone from a close friend to a financial advisor could be a good source of support.

A Coaching Session can be scheduled

Avoiding Emotional Spending is a good rule of thumb.

He argues, “A bad money habit provides immediate satisfaction and tends to satisfy short-term needs.” Keep your credit card at home and avoid going out when you’re anxious or depressed in order to limit your emotional expenditures. A few days of contemplation and budgeting will help you decide whether or not to buy something.

Use an App to Keep Track of Your Budget

There are a variety of budgeting tools available if you find it difficult to keep track of your finances. Using a budgeting programme like Mint, for example, can help you get closer to your financial objectives and develop healthier money habits. Budget software can help you keep track of your spending and make it more difficult for you to impulse buy.

Identify and Set Financial Goals

Start a habit of making a physical list of financial goals you wish to reach if you’re more of a visual learner and driven by achieving little targets. If you do this, you will have a better idea of what you should be doing and how you can go about achieving your goals.

“Good money habits help you achieve your financial goals,” according to the adage. In the words of Mint Financial Coach’s CFP, Om Mandhana:

Make Yourself a Priority Number

Changing your spending habits doesn’t mean you have to stop buying the items you want. It’s possible to have fun and save money at the same time if you prepare beforehand. Prioritize your needs before your wants,” advises Smout. Spending money on the things we enjoy is fine, but not at the risk of our future by not saving or trying to run from the past by not paying our obligations,”

Budgeting and saving regularly allow you to invest in a brighter future, take pleasure in the things you love, and provide for your loved ones.

Spending money on things we enjoy is fine, but not at the expense of our future by not saving or trying to avoid the past by not paying our obligations. — CPA Jared Smout, Mint’s Personal Finance Expert

Your role models should be reevaluated.

Your role models may be outdated if you’re constantly striving to live up to the extravagant lifestyles of celebrities and your pals. Get off social media to avoid being tempted to spend money you don’t have and surround yourself with people who will encourage you to begin developing healthier financial habits right away.

21. Make Wise Investment Decisions

If done correctly, investing can lead to financial independence, but if done incorrectly, it can lead to financial ruin. As Mandhana recommends, don’t invest in anything until you’re sure of what you’re getting your money into! Learn about investing and make sure you can afford it before making a long-term investment. The most important thing to remember when making a long-term investment is to be financially stable and to know exactly what you’re doing.

Living within your means is a good rule of thumb.

When it comes to spending, “living within your means” means spending less than you earn each month. “Whenever possible, you should attempt to spend less than your income,” Castella advises. You should strive to cut back on non-essential expenditures if you can’t afford it if you don’t want to take on too much debt.”

Being cautious while making decisions can also help you stay within your budget. “We all need hope that things will get better, but the worst money habit is to live beyond your means—spending more than you earn on the mistaken notion that things are already better.” Wait until the expected consequences have really occurred before making a choice based on them.”

Try to spend less money than you earn whenever possible. To avoid taking on too much debt, you should strive to cut back on non-essential spending if you can. The CPA and Mint Financial Coach Anthony Castella say:

Emergency Preparedness: Plan for the Unexpected

Having a plan in place in the event of an emergency can ensure that you don’t put pressure on your money. Regularly contribute to your emergency fund and set aside a portion of your monthly salary for savings. According to Mandhana, it’s important to always have enough life insurance to cover your annual living expenses for ten years, your children’s schooling, and any other outstanding loans.

Because emergencies can happen at any time, it’s a good idea to prepare ahead of time, say our experts. For example, Schule advises, “Try to anticipate the unforeseen demands of family, such as parents and siblings. Even if you have to say no, saying yes feels better.”

As much as possible, anticipate the requirements of family members, such as parents and siblings. There are times when saying no is preferable to saying yes,” he says. CPA and Mint Financial Coach Ralph Schule

The Verdict

The good news is that you’ve already taken the first step toward improving your financial habits by learning how to get started. Budgeting can be a daunting task, but integrating these strategies into your spending and saving habits will help you adapt and build an even better financial future for yourself.

The post 23 Better Money Habits You Need to Start Doing in 2022 appeared first on MintLife Blog.

The post 23 Better Money Habits You Need to Start Doing in 2022 appeared first on https://gqcentral.co.uk